In a rush to continue high income levels grain growers expect to plant a record-breaking 24.5 million hectares of winter crop

Many industry analysts have been suggesting growers are heading towards a record-high winter crop planting for season 2025-26, and Rabobank backs that scenario in its just-released 2025-26 Australian Winter Crop Outlook.

The annual outlook, prepared by the agribusiness banking specialist RaboResearch’s division, says the nation’s grain growers are expected to plant an estimated 24.5 million hectares of winter crop this year, up 0.8 per cent on last season.

The forecast increase is largely driven by good soil moisture levels in northern New South Wales and Queensland, as well as, a positive gross margin outlook, for most crop types.

Both these states are coming off near-record results from the 2024-25 winter season, and a further good run this season would set growers up on a solid footing.

Area planted to crops is expected to be up in all states, except for South Australia, where many growing regions have been struggling with severe drought conditions.

And this means SA growers are facing the same situation as last year, when the overall crop harvest was down by 40 per cent on the previous year.

And while Victorian growers were also impacted by drought in many western regions of the state last season, with the harvest down by 31 per cent, it is expected that the area planted this year could go up, but only fractionally.

The overall rise in national planted area is expected to benefit most crops, except for wheat, where area is forecast to drop, especially in Western Australia, impacted by rising fertiliser prices and less optimistic market prospects.

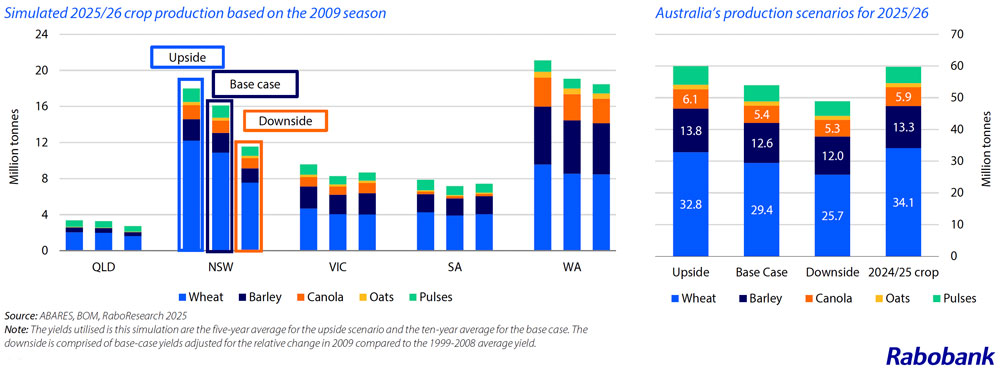

Despite the projected overall increase in the winter cropping area, RaboResearch is currently forecasting total production for the 2025-26 harvest to come in below last year’s, at a base case of 53.9 million tonnes, compared with 59.7 million tonnes in 2024-25.

Report author, RaboResearch senior analyst Vitor Pistoia is the first to suggest, the 2025-26 winter cropping area may in fact be “the largest on record” if a seasonal break comes soon in South Australia and western Victoria.

However, the impact of weather on the season ahead has led the bank to expect there could be a slightly reduced amount of grain heading to the bins at harvest time.

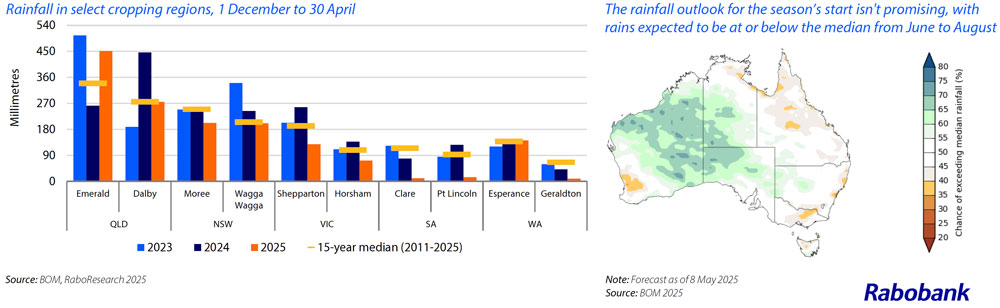

Vitor Pistoia explains his reasoning, “Summer rainfall in Queensland and northern New South Wales was above average, leading to flooding in some cropping regions, and this may delay sowing.

“But it is supportive for another season of large sowing areas. WA’s southern cropping areas also received timely rainfall to have a good start to the season.

“Other cropping regions around the country though, did not get the same summer luck. Soil-moisture levels are generally insufficient, especially in South Australia, western parts of Victoria and southern New South Wales.

“As of mid-May, the weather outlook for the season ahead is for average rainfall for the eastern states and some chance of above average rainfall for Western Australia by spring time,” Vitor Pistoia adds.

Wheat makes room for barley and pulses

Area planted to wheat is expected to decrease 5.2 per cent from the previous year, to 12.6 million hectares, with the most significant drop in wheat planting is anticipated in Western Australia, the report outlines.

“Overall, this decline in wheat planting is attributed to rising fertiliser prices and less enthusiasm about the outlook for wheat prices,” Vitor Pistoia continues.

“Crop rotation is also a factor, as last year’s late seasonal break led to wheat replacing canola and pulses at the eleventh hour, and those growers will now be looking to plant a different crop.”

RaboResearch expects cropping area for barley to increase 9.8 per cent year-on-year to 4.5 million hectares, supported by strong demand for livestock feed from the local animal protein sector.

“Despite gross margins for barley expected to be within historical averages, it is a promising outlook for regions that can achieve higher yields with barley than wheat, as the price difference between the two commodities is comparatively small,” Vitor Pistoia adds.

Canola planting is projected to remain virtually stable, with just minimal forecast area growth of 0.4 per cent on last year to 3.2 million hectares, seeing increases in Western Australia and declines in the eastern states.

“There is a supportive outlook for canola, although the price direction varies between genetically-modified (GM) and non-GM canola,” Vitor Pistoia clarifies. “Geopolitical turmoil is pressuring the GM-canola market, while demand from the EU is driving non-GM fundamentals.”

Pulse plantings are also expected to be up considerable, up by 12.5 per cent on last year to 3.4 million hectares, with Western Australia and Queensland likely to lead the expansion in pulse area.

This is driven by tariff announcements in key pulse markets – including India, a country crucial to Australian pulse exports, and that indicates demand will remain steady. “Such positive overseas’ demand signals may lead to higher margin potential compared with cereals,” Vitor Pistoia adds.

Not every cropping region has been blessed with a good rainfall forecast but that hasn’t stopped dryland growers from helping to set a planting record for season 2025-26

State by state expectations

Queensland looks to be the big winner in terms of increased cropping area, with excellent soil moisture setting the stage for a promising season, the RaboResearch report outlines.

Area under cropping is forecast to expand 8.4 per cent on last year, to a total of 1.67 million hectares.

Western Australia is expected to be the other big winner, with cropping area projected to increase 2.1 per cent to 8.83 million hectares, despite the reduction in the amount of wheat planted in the state.

New South Wales is a more mixed bag, according to the report, with positive soil moisture in the northern parts of the state, after a wet summer, driving expansion.

While cropping areas in southern regions have been impacted by low soil-moisture levels. Overall though, cropped hectares in the state are projected to increase this season by 1.6 per cent to 6.83 million hectares.

Meanwhile, dry weather in the western parts of Victoria is seeing cropping programs being diversified this season, the report indicates.

“While some Victorian growers are going for a ‘high input, high return’ approach, with crop rotation edging towards an evenly split ratio of canola and cereal cropping area, others are still using crop rotation as a tool for mitigating risk, with pulses and hay in the cropping mix as well,” Vitor Pistoia explains.

Overall, Victorian cropping area is expected to increase just 0.1 per cent on the previous season, to 3.61 million hectares.

Ongoing severe dry weather conditions in South Australia are expected to see the state’s cropped area decline this year, by 5.8 per cent to 3.55 million hectares, the report details.

However, Vitor Pistoia points out big planting shifts were also anticipated in the state, with increasing lentil planting.

“Given the average yields and current commodity price outlook, lentils offer a more attractive gross margin potential than wheat or canola in many parts of South Australia for the 2025/26 season,” Vitor Pistoia adds.

Market outlook and exports

In terms of market outlook, the report indicates that despite the US’s tariff-driven efforts to re-order global trade, Australia’s key grain and oilseeds exports seem largely unscathed for now and may gain global market share”.

“Asian countries rely on Australia to source imports of grains and pulses, and the EU imports canola to balance its supply of oilseeds,” Vitor Pistoia quantifies.

The report outlined that Australia exported most grains and oilseeds at a good pace in early 2025, although not wheat. Wheat export volumes from October 2024 to March 2025 reached 9.9 million tonnes, alling 3.1 million short of the pace needed to avoid an increase in year-on-year carryover stock.

A larger carryover would make the ASX (Australian Stock Exchange) wheat futures prices softer compared with the global CBOT (Chicago Board of Trade) and MATIF prices, the report outlines.

Globally, with increased wheat supply from the EU and another robust Black Sea crop likely, there are not many reasons to be bullish on wheat prices, the report suggests.

For local growers, RaboResearch forecasts APW port prices to range between AU$330 and AU$360 per tonne by the end of 2025, partially supported by currency headwinds.

Feed barley prices for the 2025-26 harvest are anticipated to range between AU$290 and AU$340 per tonne, the report estimates, depending on the volume of new crop production.

On the malting barley front, there is limited upside beyond Chinese demand, RaboResearch indicated, with prices projected to be AU$10 to AU$20 per tonne higher than feed barley.

Canola prices are expected to soften by mid-year as harvests begin in the northern hemisphere. “If EU production falls below 18 million tonnes, Australian non-GM port prices for the 2025-26 season are likely to stay within the AU$700 to AU$780 per tonne range, with an eight to 12 per cent discount for GM canola,” Vitor Pistoia concluded.