Net sales of US$2.6 billion for the Q2 2025 represent an 18% decrease for the same period last year and an improvement on the Q1 30% drop

AGCO second-quarter sales worldwide, ending 30 June 2025, revealed a decrease of 18% when compared to the second quarter of 2024. However, an improvement on quarter one sales where a 30% decrease was recorded. See Q1 story here.

For the manufacture and subsequent distribution of agricultural machinery and precision ag technology, reported net sales were US$2.6 billion for the second quarter of 2025.

The company also makes the point that second quarter of 2024 income was slightly inflated as it included other revenue of US$290.5 million, representing revenue from the Company’s divestiture of the majority of its Grain & Protein business.

This result places net sales for the first six months of 2025 at approximately US$4.7 billion, which represents a decrease of 24.1% compared to the same period in 2024.

AGCO CEO steps up

“AGCO achieved solid second-quarter results with deliberate execution in the areas we can control despite a challenging global agricultural environment marked by weak farm economics and delayed purchasing decisions in several parts of the world,” outlined Eric Hansotia, Chairman, President and CEO.

“Our strong earnings and cash flow generation illustrate meaningful progress in reducing dealer and company inventories through aggressive production cuts. Operating margins benefited from disciplined cost control and continued implementation of our restructuring initiatives.

“Demand for our premium brands remains resilient, supported by growing interest in precision agriculture and sustainable technologies.

Eric Hansotia continued, “The global trade landscape has become increasingly complex, with uncertainty surrounding trade negotiations impacting farmer confidence and investment decisions, particularly in North America and Europe.

“AGCO is closely monitoring these developments and remains focused on operational agility, supply chain resilience and executing our Farmer-First strategy.

“Challenging farm economics in the first half of 2025 have dampened demand for agricultural equipment across Europe and the US, with declining commodity prices and rising input costs specifically impacting US farmer sentiment. Instead, there is growing interest in precision agriculture tools that offer efficiency gains without significant capital investment.

“In Brazil, erratic weather and lower prices have made farmers more cautious, with many choosing to maintain existing equipment rather than invest in new high-power machinery.

“In Europe, environmental regulations and weather-related disruptions are driving demand for sustainable and adaptive technologies. While traditional equipment sales remain under pressure, we are seeing a clear shift toward smarter, more efficient solutions as farmers work to protect margins and navigate ongoing volatility,” Eric Hansotia concluded.

How world regions fared

North American industry retail tractor sales declined 13% in the first half of 2025 compared to the same period in 2024 with the steepest drops occurring in higher power categories, particularly in recent months. Combine unit sales fell 33% year-over-year during the same period. Ongoing uncertainty around grain export demand and elevated input costs are expected to continue weighing on industry demand throughout 2025, especially for larger equipment.

Brazil industry retail tractor sales rose 6% in the first half of 2025 compared to the same period in 2024, driven primarily by demand for smaller tractors. Despite record soybean harvests and potential trade benefits, demand for larger equipment has yet to show meaningful improvement. If trade conditions continue to strengthen farm economics, demand could pick up later in the year. For now, industry growth in Brazil is expected to remain modest.

Western Europe industry retail tractor sales declined 12% during the first six months of 2025 compared to the same period in 2024 with double digit percentage decreases across most markets except Spain and Italy, which both saw modest growth. Demand is expected to remain soft throughout the year, as lower income levels weigh on arable farmers. However, steady demand from dairy and livestock producers is expected to partially offset the overall decline.

Regional Results

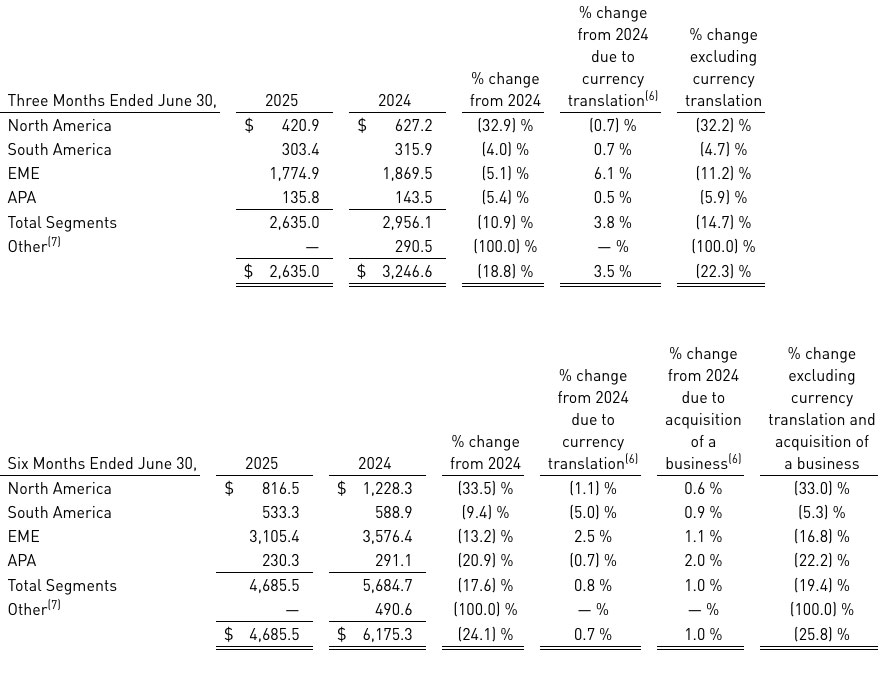

AGCO Regional Net Sales (in US$ millions)

(7) “Other” represents the results for the three and six months ended June 30, 2024 for the majority of the Company’s Grain & Protein (“G&P”) business which was divested on November 1, 2024. The results of the G&P business through the date of the divestiture were previously included within our North America, South America, Europe/Middle East and Asia/Pacific/Africa segments.

North America

North American net sales decreased 32.2% during the second quarter of 2025 compared to the second quarter of 2024, excluding the impact of unfavourable currency translation. Softer industry sales and under-production of end-market demand contributed to lower sales. The most significant sales declines occurred in high-power tractors, sprayers and hay equipment.

Income from operations in North America for the second quarter of 2025 decreased US$58.3 million compared to the same period in 2024, and operating margins were (5.3)%. The decrease was primarily a result of lower sales and production volumes.

South America

Net sales in the South American region decreased 4.7% during the second quarter of 2025 compared to the second quarter of 2024, excluding the impact of favourable currency translation. Dealer inventory de-stocking drove most of the decrease. Lower sales of mid-range tractors, planters and sprayers accounted for most of the decline.

Income from operations for the second quarter of 2025 increased US$17.4 million compared to the same period in 2024. This increase was primarily a result of improved product mix and improved factory efficiency, partially offset by negative pricing impacts.

Europe/Middle East

Europe/Middle East region net sales decreased 11.2% during the second quarter of 2025 compared to the second quarter of 2024, excluding the impact of favourable currency translation. Lower sales across most of the Western European markets were partially offset by growth in Eastern Europe and Scandinavia.

Declines were largest in high-power tractors and combines. Income from operations decreased US$34.3 million in the second quarter of 2025 compared to the same period in 2024. This decrease was primarily a result of lower sales and production volumes as well as higher warranty costs.

Asia/Pacific/Africa

Net sales in the Asia/Pacific/Africa region decreased 5.9%, excluding favourable currency translation impacts, during the second quarter of 2025 compared to the second quarter of 2024 due to weaker end-market demand and lower production volumes.

Lower sales in Australia, China and Japan drove most of the decline. Income from operations decreased US$1.0 million in the second quarter of 2025 compared to the same period in 2024, primarily due to lower sales and production volumes.

Outlook from AGCO

AGCO now expects full-year 2025 net sales of approximately US$9.8 billion. Adjusted operating margins are projected to be approximately 7.5%. Lower production volumes are expected to be partially offset by cost controls and stable engineering expenses. Based on these assumptions, full-year earnings per share are now targeted between US$4.75 and US$5.00. These estimates incorporate the expected impact of tariffs in effect as of 31July 2025, along with AGCO’s mitigation strategies. Any changes to tariff policies or related responses could affect these projections.