Livestock and global dairy prices lift at the same time as winter crop prospects are boosted by good rainfall to give producers greater confidence heading into spring

Rural Bank has provided an analyst into what is a quickly increasing in volume agricultural market where most sectors can expect very healthy returns for the 2022-23 season.

Livestock prices are recovering quickly following patchy downturns during winter. While global dairy prices also posted a lift in early September. This follows a sustained downturn since March.

Winter crop prospects were further boosted by good rainfall in August. Current estimates place 2022-23 production as the fourth highest on record, with the chance of an even higher mark before season end.

Take a look at the summary of predictions for the main farm sector incomes and see what returns producers can expect heading into spring.

Winter crops in near record territory

Growers are on a winning streak as beneficial rainfall during August has improved the chances of another high-volume winter crop harvest.

National wheat production in early estimated sits at 32 to 33 million tonnes.

In addition, barley production is forecast around 12 million tonnes and canola at six million tonnes.

Climate models continue to predict a very high chance of above median rainfall over the next three months for a large part of eastern Australia.

Soil moisture levels are currently high throughout Queensland and New South Wales. This makes excessive rainfall during harvest the biggest threat for these regions.

Australian exports remain strong on continued demand from Asia. Despite supply chain bottlenecks, 36Mmt of grain has been exported to the end of August.

This exceeds last year’s record of 32Mmt. And another 2.9Mmt remains booked for the final month of the marketing year. On the domestic front, end users appear well covered as they wait for new season harvest to start.

The resulting sluggish market has given sellers little incentive to make a move on new crop sales. A much smaller tonnage has been forward sold so far compared to this time last year.

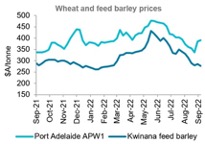

International wheat futures have softened since the peak in mid-May.

In August, Chicago wheat bottomed out at A$388 per tonne, the lowest level since January. The resumption of bulk exports out of Ukraine is one contributor to easing prices. Another is the US spring harvest which has alleviated some immediate supply pressure.

But international prices are still at levels not seen before late last year. Even with the resumption of Black Sea exports, global stocks remain tight and are supporting global prices.

Australian prices have softened substantially since May, following the lead of international prices.

The season ahead provides indications of similar pricing conditions to the past season. Tight global stocks will see strong export demand for Australian grain. But a large crop and supply chain constraints will limit upside potential.

This means we are likely to see basis remain negative through the upcoming season. Australian grain prices will face downwards pressure as harvest progresses.

Prices are expected to remain above average throughout the season. But given high input costs, whether prices will be high enough to cover cost of production may come down to yields achieved for small operations.

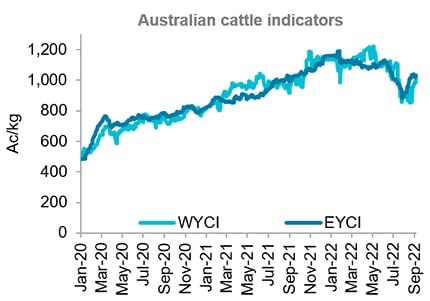

Cattle prices in upward trend

Producers reap the benefits as local cattle prices have trended higher over the past month.

The Eastern Young Cattle Indicator (EYCI) reached 1,033c/kg, a 16.5% recovery from a low in late-July. The EYCI has also risen to be 3.5% higher year-on-year.

The Western Young Cattle Indicator was also firmer in August, rising by 8.9% to end at 1,002c/kg. This was 5.9% higher than this time last year.

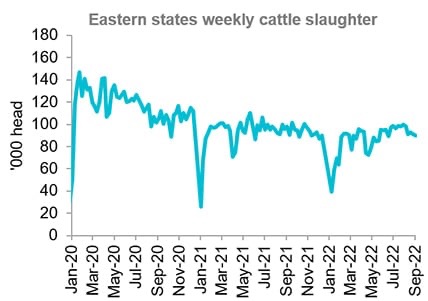

A decline in Australian cattle slaughter over the past month helped support higher prices. Eastern states slaughter in the first week of September was 8.5% lower than a month earlier.

A contributor to this decline was rainfall continuing to arrive in August across most cattle producing regions.

The favourable seasonal conditions which are forecasted in the coming months could see slaughter rates remain well below average for the next month.

In addition, several beef processors remained constrained by logistical challenges and labour shortages in August. This also contributed to the lower slaughter rates.

August was a strong month for Australian beef exports. Export volume rose by 22.9% from July and was 19.4% higher year-on-year.

Japan continued to be Australia’s largest beef export market and had a 19% rise month-on-month. However, total exports for the year-to-date were down 4.8% from 2021.

The liquidation of the US cattle herd has seen competition into the Japanese market increase. This competition is expected to continue in September as the US continues to provide an abundance of grain fed beef to the market.

Exports to China rose by 34% in August to over 16,000 tonnes. This was 41% higher when compared to August 2021.

Year-to-date exports to China are up 6.3% in 2022 but Australia continues to face strong competition from cheaper South American and US supplies.

Exports to South Korea were boosted by the recent removal of the 16% tariff. This was removed to combat inflation and soften prices. This helped exports in August to climb 22.4% month-on-month, placing them 42.5% higher than a year ago.

Australian beef prices are expected to rise throughout the next month as supply shortages, below average slaughter rates and favourable seasonal conditions in cattle producing regions apply upwards pressure on prices.

Dairy prices lifting on global market

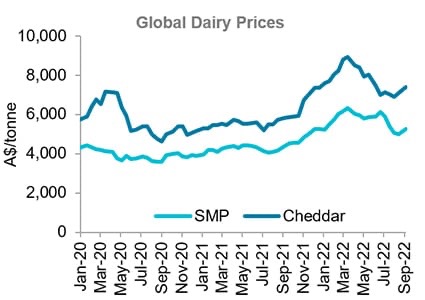

Dairy producers are looking at steady returns as the global dairy markets showed a sharp improvement at the start of September following a sustained downturn since March.

The first Global Dairy Trade (GDT) auction of September saw the GDT Index rise 5%. This was only the second rise in the Index since March.

Despite this rise, the Index is still 25.6% below its peak in March. Both skim milk powder (SMP) and cheddar prices are still down 22% from March. The recent lift in the market was largely due to firmer Chinese demand which had been weaker in recent months.

Downward pressure will likely remain on prices due to softening consumer demand. Chinese demand remains somewhat weakened by ongoing COVID control measures.

Consumer demand in other markets could also soften under pressure from rising costs of living. These factors led to Fonterra dropping their forecast New Zealand farmgate milk price by 25c/kg MS in late August.

At the same time, global milk supply remains tight which will offer ongoing support to prices. New Zealand production declined by 5.5% in July and is forecast to be 2.2% lower this season.

European production is also facing dry conditions which are preventing growth. Tight supply is evident in SMP and cheddar prices sitting above five-year averages by 28% and 21%, respectively.

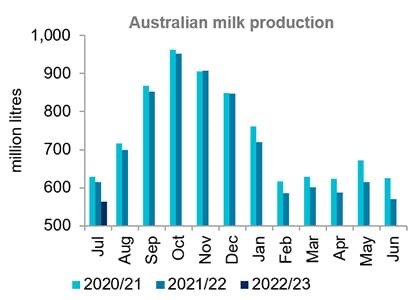

Local milk production is also contributing to tight global supply. June production was 8.8% lower year-on-year which saw the 2021/22 season finish 3.4% lower than the prior season. At 8.5 billion litres, production in 2021/22 was just below average.

Adverse weather events in some regions and further industry exits saw production fall well short of initial growth estimates of up to 2%. Tight supply continued into the new season.

July production down 8.3% year-on-year and 10.1% below the five-year average for July. Growth compared to last season is unlikely.

High input costs, labour availability and challenges from wet conditions will continue to hamper growth and confidence to expand output.

Tight milk supply in Australia drove the high farmgate milk prices currently being received by farmers. With those prices locked-in for the season and movement in global markets, processor margins will be under pressure.

For producers, high input costs will also continue to challenge margins and mitigate some of the benefits of higher farmgate prices.

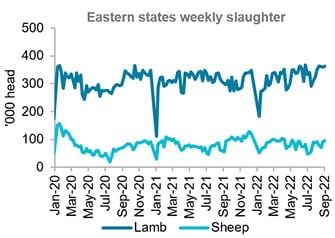

Lamb and sheep prices recover

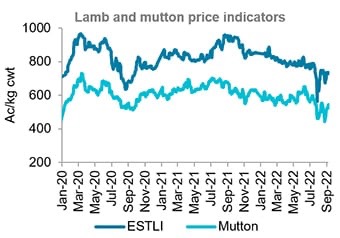

Lamb and sheep prices staged a recovery during the past month following a sharp decline in late July.

After spending some weeks below 700c/kg, the Eastern States Trade Lamb Indicator (ESTLI) returned above that mark in August. Similarly, mutton prices dipped below 450c/kg but have since risen above 500c/kg.

Prices recovered on the back of renewed competition at saleyards. Competition had been lacking as winter maintenance closures say some processors absent from markets.

Buyers have returned to saleyards in greater force and the quality of lambs has improved, further assisting prices. It is a different story in Western Australia where trade lamb prices remain subdued. At 539c/kg, Western Australian trade lambs hold a 27 per cent discount to the ESTLI.

While prices have recovered, most lamb categories remain 20 to 30% lower than a year ago. This is largely the result of increased supply.

Eastern states lamb slaughter in the first week of September was 20.6% higher year-on-year.

Weekly slaughter has been above 360,000 head for four weeks in a row now. That level of weekly slaughter has only been achieved in three other weeks since the end of 2019.

Increased supply has come from consecutive years of flock rebuilding activity. Lamb supply is expected to remain elevated for the remainder of the year as the spring flush of new season lambs come onto market.

Sheep slaughter has also started to trend higher. However, weekly slaughter in the first week of September was still 18.4% below the five-year average.

Increased lamb slaughter translated into increased export volumes. The volume of lamb exports in August was up 4% from July and 12.8% higher than a year earlier.

Strong demand continued to be led by the US. Exports to China have steadily grown recently with volumes in August up 42% from March. Despite this improvement, year-to-date exports to China are 27% lower year-on-year.

Strong growth in export volumes has also been seen to South Korea, Papua New Guinea and Malaysia. Mutton exports also increased in August with a 45% rise from July. Growth was led by China who typically import the majority of their mutton in the second half of the year.

Lamb and sheep prices are expected to show some stability in the coming month. Supply set to rise as new season lambs enter the market in greater numbers. However, this should be matched by firm restocker demand and underpinned by strong export demand.

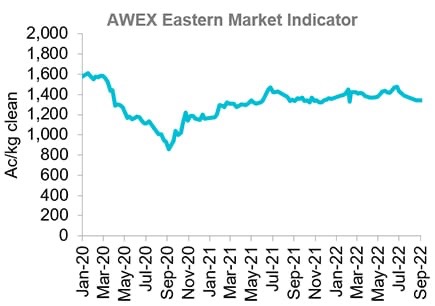

Wool production continues to increase

Australian wool production is on the rise. The Australian Wool Testing Authority reported that testing volumes in August were 11% higher year-on-year.

This is reflective of Australia’s increasing sheep flock and increased cuts per head. Meat and Livestock Australia project the flock to reach 78.8 million next year. This represents a marked increase since mid-2020 when the flock was 64 million.

At that time the Eastern Market Indicator (EMI) was almost 20% higher. The increasing flock size is indicative of confidence in the sheep meat industry and strong seasonal conditions driving higher lambing rates across Australia.

While the supply of wool in August has strengthened, prices continued to be the victim of economic headwinds. The EMI has fallen to 1,330c/kg which is the lowest level in 10 months. This comes after a few months of being relatively solid at 1,400c/kg.

During August sales, price discounts for fine wool lead the decrease with medium wool remain largely firm for the month. 17-micron wool is currently down 171c/kg when compared to the closing price before the winter sale break.

Crossbred wool has also continued its long-term decline finishing at 380c/kg. This is lowest 28-micron price in over 20 years placing more pressure on shearing costs for growers.

The Australian dollar regained some value in the beginning of August before falling to 68.8 US cents in the start of September.

In US dollar terms the EMI is now trading at its lowest value since January 2021 at just 915 USc/kg. This is a stabilising factor for wool as the market faces other challenges abroad.

Softer demand in August was driven by uncertainty surrounding future consumer demand in the face of economic headwinds.

As wool buyers grow apprehensive, and the supply remains strong the premiums for quality wool become stark. This has laid bare the price premiums of Responsible Standard Wool (RWS).

The take up of the industry standard has increased three-fold since the beginning of 2022. The price premium has been up to $3/kg in some lots.

At this point the supply of such wool remains relatively scarce with mulesing remaining the dominant practice in the merino wool industry.

China’s ban on South African wool imports has finally lifted after an embargo was enacted earlier in the year. The South African wool industry has faced Chinese trade restrictions twice in the last three years due to local outbreaks of foot and mouth disease.

The peak wool body in South Africa estimated that the ban cost the industry over AUD$60 million in wool exports to China. During the ban, South African wool has been trading into Europe and India for large discounts. The spectre of biosecurity threats still looms over the confidence of some buyers and growers locally.

Horticulture prices high but with increased input costs

It depends on what sector you are harvesting as to how growers are faring during a long winter period that impacted negatively on supply

Fruit

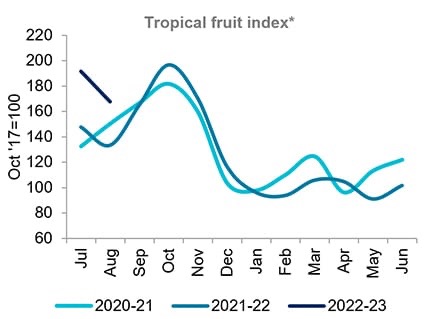

Fruit prices are on the rise again as labour shortages, input costs, and pollination challenges weigh on grower margins. Some reports are indicating costs for producers have risen by more than 40% over the last couple of seasons.

Banana prices are now increasing as a long winter continues to impact supply. This is now pushing prices back to the point of profitability for growers. Prices have risen by more than 11% over the last month.

These higher prices will remain throughout September before the warmer weather increases volumes. Stone fruit producers are also warning of higher prices. Difficulties sourcing bees for pollination and a wet spring are expected to impact production and quality.

Northern Territory mango growers are also anticipating a large crop this season. There are 2.7 million trays of mangos currently forecast, 300,000 trays more than last season.

Labour shortages remain a concern with the sector still 1,000 pickers short and harvest due to peak in October. This shortage of workers may even see a portion of the crop left unharvested.

Vegetables

Prices are expected to continuing easing over the coming months as supply issues related to weather events on the east coast improve.

Despite this, high input and freight costs combined with labour shortages will see prices remain above average for the short term.

As a result, an increasing number of consumers are switching to frozen vegetables to combat the rising cost of living. This trend is expected to continue over the coming months.

Nuts

The Australian Macadamia society have released updated production forecasts with harvest now over 90% complete.

Production estimates of 49,340 tonnes (in shell 3.5% moisture) are on track to be met. This follows a cut to forecasts earlier this year after weather events across key production regions.

Quality remains strong across most regions following some dry weather throughout July and August. The pollination of almond plantations is continuing.

This is despite the restriction on beehive movements imposed by the Victorian government following the varroa mite outbreak in July.

More than 80,000 beehives have been moved into southern New South Wales to pollinate the almond crop. This has come as a large relief to growers across the region.

Should pollination continue without any major hiccups another large almond crop will be on the horizon. This is driven by the maturation of newer plantings and low irrigation costs to hold crops in good stead.

* The tropical fruit index includes bananas, mangoes, papaws, passionfruit and pineapples.

Sources: Ausmarket Consultants, Rural Bank