However the longer-term outlook is more positive as a decline in US supply could provide greater export opportunities

Analysts are tipping cattle prices will remain under some downward pressure for the next few months, and for many, that’s simply a continuation of the steady decline seen in recent weeks according to Rural Bank.

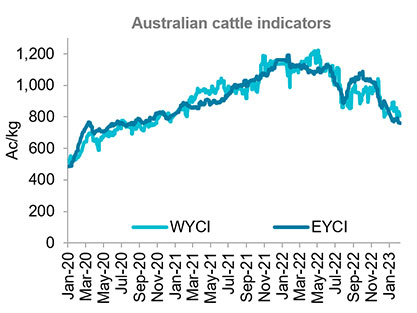

The Eastern Young Cattle Indicator (EYCI) is currently 755c/kg. This is only 2.9% lower than at the start of 2023, suggesting the market is finding some stability following the rapid decline in late-2022.

The recent range of the EYCI is around 30% lower than when the price decline started in October 2022. This has brought the EYCI just below the five-year average.

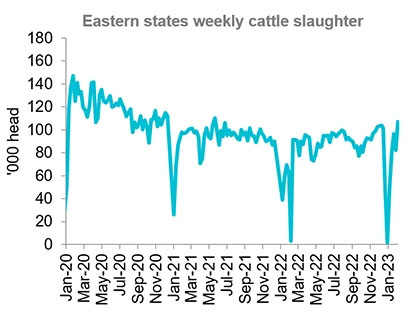

Downward pressure on prices is expected to continue coming from the increasing supply. The start of February saw weak eastern states’ cattle slaughter rise to just over 107,000 head. This was the highest weekly slaughter since May 2021 and represents a 33% rise since early October.

Slaughter in all states except for South Australia and Western Australia is sitting higher year-on-year. This is a feat rarely seen in the last two years.

Despite the increase in recent months, the latest weekly slaughter was still 5.8% below the five-year average. Slaughter will continue to rise and close in on average levels.

It is expected strong competition in international markets will also weigh on prices in the short term. Increased slaughter helped drive export volumes 9.1% higher in December. This made December the second-largest export month for 2022.

However, weaker global markets saw the average price of Australian beef exports fall 5.5%. This was the lowest point since November 2021.

Lower pricing for exports is also reflected in the US lean beef import price. This price has fallen 19% since October and hit its lowest point since April 2021. This was due in part to both weaker US demand for imports and also appreciation in the Australian dollar.

There is light at the end of the tunnel as it is expected an inevitable slowdown in US production should ease competitive pressures later in 2023.

The US cattle herd has shrunk by almost six per cent since the start of 2019 and is at its lowest point since the 1960s. This will keep US production heavily constrained for the next few years.

And as a result, will open greater export opportunities for Australian beef in the US. Reduced US exports will also allow Australia to recapture market share in Japan and South Korea.