A recent report indicates fertiliser prices that shot through the roof last season could return to more affordable levels as several factors kick in

Growers appear to be clinging to the hope that farm fertiliser affordability is starting to improve across the globe, with a likely recovery in some world markets later in 2023.

This is what Rabobank experts predict for the future in a recently released report. However, the report is prefaced with suppositions and confirms that in most cases, demand will take some time to return to pre-pandemic levels.

The global agribusiness banker says most fertiliser prices are gradually returning to their historical averages, after skyrocketing over the past two years due to the impacts of Covid-19 and the Russia-Ukraine war.

The report outlines how global fertiliser prices began to trend higher in 2021 due to supply chain constraints resulting from the Covid-19 pandemic.

Affordability deteriorated further when fertiliser prices set new record-high levels after Russia invaded Ukraine, reducing supply from the region and also resulting in higher production costs.

By that time, Rabobank analyst Vitor Pistoia explained, “Reasonable prices for agricultural commodities were the only reason fertiliser didn’t become as unaffordable as it was in 2009 during the global economic crisis”.

“Prices continue to remain above average for a number of agricultural commodities, due to tighter stocks.

“The combination of still-positive commodity prices and lower fertiliser prices is helping fertiliser affordability for farmers. Although globally, ‘consumption’ may take two or three years to recover, and the speed of recovery will depend on how long the current positive cycle lasts,” Vitor Pistoia added.

Local growers’ position

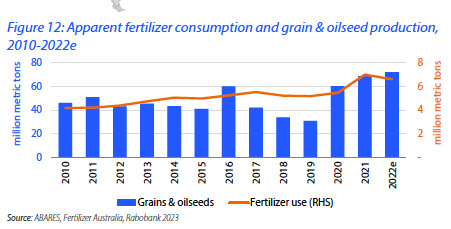

For Australia, the Rabobank report indicates how in recent years fertiliser demand has grown despite the price hikes, as growers enjoyed good seasonal conditions and a surge in grain and oilseed production.

“Every year since 2020, G&O (grain and oilseeds) yields have exceeded the previous year’s production, with 2022 winter and summer crop seasons combined reaching a historically high 72 million metric tonnes, a 130% surge,” Vitor Pistoia continued.

At the same time, the cropping area increased 27% from around 20 million hectares to 25.5 million hectares, the report concluded.

Vitor Pistoia outlined how good weather driven by La Nina and investments in crop management had underpinned this “phenomenal growth”.

Apparent fertiliser demand in the same period moved from 5.4 million to around 6.6 million metric tonnes, a 21% increase, according to the report.

“Although the conditions for the 2023 crop seasons are a bit different, they do not signal a reversal in the trend of historically-high cropping area and a significant application rate,” Vitor Pistoia continued.

“The drop in farm input prices is greater than that of commodity prices, and this is slowly improving growers’ buying power,” Vitor Pistoia concluded.