Most farmers expected to leave the slippery muddy conditions they endured throughout winter far behind but malingering spring precipitation is reinforcing nature is the boss

Grain growers and livestock producers find themselves facing a minor quandary as to what brand of umbrella to buy as the wet winter unfolds into a storm laden spring.

And along with it comes a mixture of blessings and challenges as stubborn rain clouds appear difficult to budge.

On a positive note, the harvest of what could still be a record winter crop is underway in drier parts of the country.

And while this excellent growing season will deliver strong yields, quality is the only leveller for record returns for many growers.

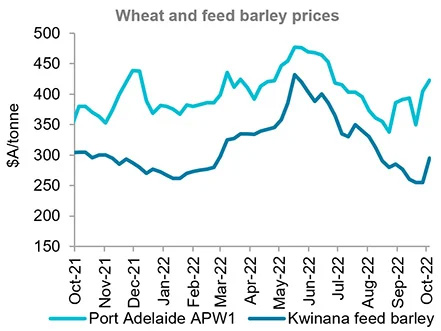

As growers keep an eye on the heavens above, they will be pleased to see the upward support for prices. Global supply concerns and currency shifts have worked in local growers’ favour with Australian wheat prices improving in the past month.

Spring also means a lift for livestock producers through their new lamb supply. Lamb prices have held up well in the past month as yarding’s increased.

However, with greater numbers of new season lambs still to come there is expected to be some downside to prices for late entries into the market.

Should this persistent wet weather continue, it will negatively affect supplies of cattle, dairy, and wool. The wet outlook, should it continue will bring further challenges to these industry sectors over the next month.

Rural Bank staff provide an analysis and insight into how they expect production and price trends to fare in the various rural sectors this spring.

Grain harvest will be big

The ongoing rainfall combined with a wet outlook for spring is causing concerns around the quality of the 2022-23 winter crop.

As local wheat growers find support from international markets with price rises of $13 to $48 per tonne in the past month.

Harvest is underway in Queensland, Western Australia and South Australia.

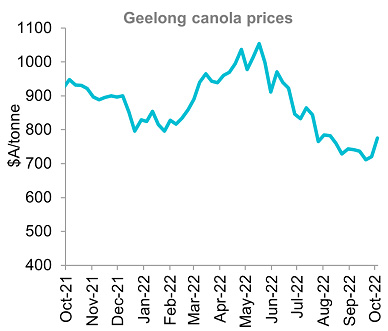

Early results show good yields for central Queensland wheat and high oil content for Western Australian canola. Wet and mild conditions mean harvest is behind schedule across the country.

As such, the bulk of the crop is still a few weeks off being ready to harvest.

The main area of concern around the crop is from persistent rain causing water logging along with quality issues as we head into harvest.

New South Wales is the state most affected with parts of Queensland and Victoria also experiencing some issues.

Hay Australia report that a high number of growers are responding to these adverse conditions by spraying out or ploughing in vetch crops.

Despite these ongoing concerns local growers are still on track to produce a very high volume winter crop.

National wheat production is estimated at 33 million tonnes. Barley forecast is at around 12 million tonnes and canola at six million tonnes.

Australian Bureau of Statistics (ABS) export data is showing combined wheat, barley and canola exports for 2021-22 to come in at over 40 million tonnes. This beat the previous year’s record of 35.9 million tonnes by 14%.

Strong demand from exporters for shipping capacity suggests export pace will remain high through the coming season. Viterra held its recent export capacity auction where records were broken.

South Australian exporters have forward booked seven million tonnes of shipping capacity from the 2022-23 season. While in Western Australia the forward stem is showing four million tonnes of grain scheduled for shipment in October and November.

International wheat futures have continued to rise over the past week and are now hovering around the highest level since the end of June. This comes amid concerns over lower world-wide supply.

The USDA’s Small Grains Summary surprised the market by cutting US winter crop production. Further escalation of the war in Ukraine is also lending negative support.

There are concerns that Moscow could suspend the safe trade corridor from Ukrainian Black Sea ports that was agreed to in a United Nations-brokered deal.

With this combination of events in the Black Sea, ongoing concerns over global wheat availability and currency shifts, Australian wheat prices have found support from gains in international markets with local wheat values up by $13 to $48 per tonne in the past four weeks.

Market concerns around the quality of our 2022-23 winter crop is also being reflected in prices. Buyers have been adjusting grade spreads and increasing premiums for higher protein wheat.

Sources: Profarmer Australia

New season lambs coming to market

Lamb supply will be the pivotal market factor through to the end of 2022.

Supply is set to build upon an increase in lamb yardings in September as new season lambs come onto the market in greater force. Average weekly lamb yardings in September were 19.1% higher than August. This was despite public holidays reducing working days later in the month.

The uplift in yardings was driven by New South Wales where average weekly yardings rose 18% from August. New South Wales yardings typically taper off after September while Victorian and South Australian yardings accelerate.

This leads to national weekly yardings rising 61% from September to December based on 10-year averages. In Victoria, yardings can quadruple from September to December.

While yardings rose in September, lamb slaughter slowed. National lamb slaughter averaged 377,429 head in September, down 6.1% from August.

Meanwhile, weekly sheep slaughter trended higher in September and exceeded 100,000 head for the first time since June.

Combined lamb and sheep slaughter reached a new high for 2022 of 518,147 in mid-September. This is 72,000 head, or 13.9% below the highest weekly slaughter between October and December achieved in the last five years.

This suggests processing capacity is holding up well so far but will need to increase as more lambs become available across the next few months.

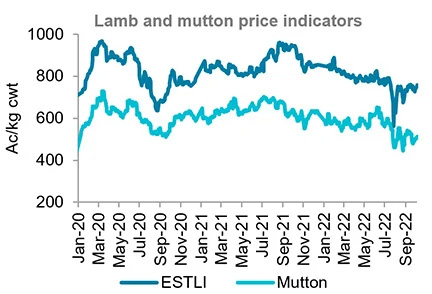

Lamb prices have held up well under the weight of increased yardings but will come under pressure as supply increases. The Eastern States Trade Lamb Indicator (ESTLI) fluctuated between 727-759c/kg in the past month.

Restocker demand has strengthened in the past month. This is evident in the national restocker lamb indicator rising 42% from a suppressed point in late-August. Light and merino lambs have also risen strongly in that time with gains of 30% and 24%, respectively.

Despite those gains, all national lamb indicators are between 19 to 23% below the same time last year. Lamb prices are also 2 to 8% below five-year averages.

Mutton prices have been fairly volatile in recent months and have generally trended lower. At 512c/kg, the national mutton indicator is currently 12.6% lower than a year ago and 6.6% below the five-year average.

Lamb and sheep prices flowing through to producers are expected to ease through to the end of the year as supply increases.

Source: Meat & Livestock Australia

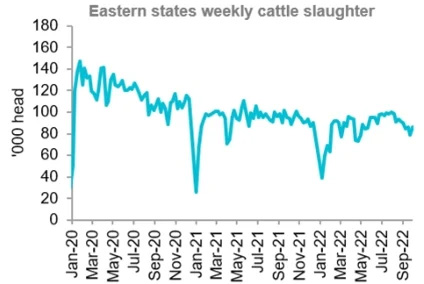

Cattle prices trending higher

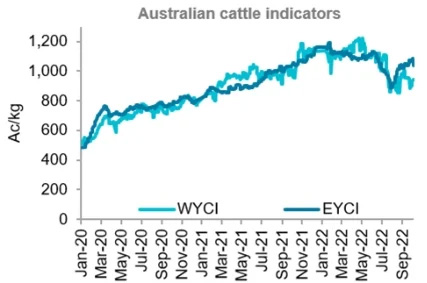

Producers watched closely as cattle prices trended higher in the past month. The Eastern Young Cattle Indicator (EYCI) reached 1,076c/kg in mid-September before softening to 1,039c/kg in early-October.

This fluctuation arose following the trend in slaughter rates which fell during the middle of September. The EYCI is currently 1.5% lower than a year ago.

The Western Young Cattle Indicator experienced a softer month, falling 5.7% to 944c/kg. This was still 2.3% lower year-on-year. Favourable seasonal conditions in many regions encouraged firmer restocker demand.

This helped fuel cattle price rises in September. Good pasture availability and a wet outlook is likely to encourage producers to continue to rebuild herds.

Cattle slaughter declined throughout the past month. Nationally, weekly slaughter was 6% lower month-on-month and 5.2% lower than a year ago.

Victorian cattle slaughter remained relatively stable with a marginal fall of 0.4%. While New South Wales and Queensland slaughter fell 10.1% and 5% respectively. This was largely due to excessive rainfall limiting the movement of stock to abattoirs.

Reduced cattle slaughter will likely see reduced beef export volumes. Exports will also be met by weakened demand. A contributor to weaker demand is the impact of China’s continued lockdowns. In addition, competition from the US has increased in key export markets.

Cattle prices are expected to marginally rise throughout the next month. Firm restocker demand is likely to persist following wetter than average seasonal conditions.

Good pasture availability will also contribute to tight supply. Producers will likely seek to retain stock and add weight to cattle. Tight supply and firm restocker demand should support some upside to cattle prices in the near-term.

Source: Meat & Livestock Australia

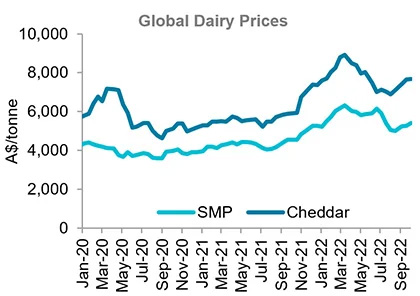

Support for dairy prices at above average

Dairy market seems harder to predict with prices declined at the first Global Dairy Trade (GDT) auction of October with major commodities losing the gains they made in September.

The GDT Index declined by 3.5% after rising by 7% across September’s auctions. The declines were attributed to weaker Chinese demand which had helped buoy the market in September. T

he Index remains relatively high at 6.4% above the five-year average but is now 5.1% lower than a year ago.

Skim milk powder (SMP) prices continued to slump, falling below US$3,500/tonne for the first time since October last year. Despite this, SMP prices are still 23.9% above the five-year average.

Cheddar prices have fared relatively better in recent auctions and currently sit 15.6% higher year-on-year. A lower exchange rate has aided dairy prices in Australian dollar terms with cheddar up 29.7% year-on-year and SMP up 18.4%.

Tight global milk production continues to support dairy prices at above-average levels. New Zealand milk production remained subdued in August, down 4.9% year-on-year. The EU saw some improvement in milk production in July with a 0.5% lift from a year earlier.

However, dry conditions are forecast to restrict any significant growth for the time being. The US is bucking the trend with a 1.6% year-on-year increase in August milk production.

US production in the final quarter of 2022 is forecast to be 1.3% higher than a year earlier. Without any significant growth in supply from major exporting nations, global diary prices should remain reasonably supported.

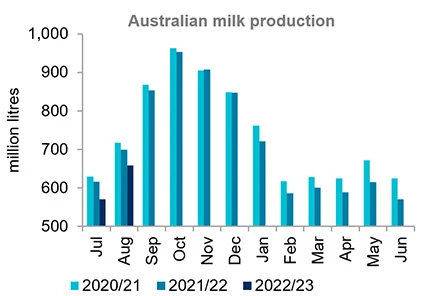

Local milk production rose by 15.4% in August. However, August production was still down 5.9% year-on-year and 7.9% below the five-year average for August.

This continued the slow start to the season seen in July. Season-to-date production is 6.6% lower than last season and 8.5% below average.

The trend of tight supply is consistent across all major production regions as excessive wet weather, labour availability and input costs are challenging milk output. This is most evident in the north coast of New South Wales. In this region, season-to-date production is 20% lower than last season.

Eastern Victoria has also seen a significant decline in production this season, down 8.4% from last season.

Production is expected to rise in-line with the typical seasonal pattern. This pattern sees national milk production increase 37.8% from August to a peak in October. And while production may increase in the next few months, it is likely to remain subdued compared to last season and average levels.

While tight supply is supportive of global dairy prices, demand is likely to soften. Chinese demand is the primary source of weakness for global markets. Chinese production and inventories are strong while consumer demand has softened. This has reduced the need for imports and weakened overall global demand.

Sources: Global Dairy Trade, Dairy Australia

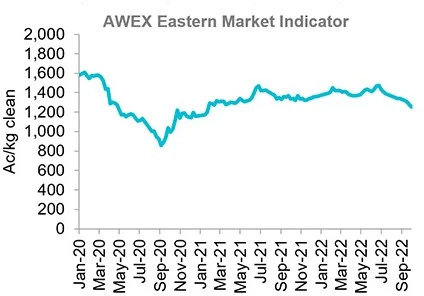

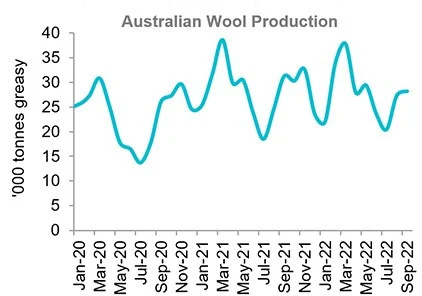

Wool prices under pressure as 17-micron falls

Global economic challenges have taken a toll on all Micron Price Guides (MPG) throughout September. This, despite a depreciating Australian Dollar and low offerings at auction.

The pass in rate climbed to 16% per cent in the last week of September as growers responded to the weakening demand across the MPGs.

The price for 17-micron wool has now fallen for eight consecutive weeks to a low of 2,352c/kg. Discounts to fine wool are coming off the back of an abnormally strong two years of sales. While medium wool has been relatively solid during September, the value of 21-micron wool has fallen 15% since June.

This compares to a 16% drop of 17-micron wool during the same period. There has been no reprieve for 28-micron wool which has once again fallen to its lowest price in over 20 years.

A 5kg fleece of 28-micron wool now has a market value of $11 which is not likely to cover costs associated with shearing and selling.

The Australian Wool Testing Authority tested 148,000 bales during September which is down 26,000 on the same month last year. Wet weather across the eastern states is causing delays in shearing which is impacting supply while staples continue to grow.

Average tested staple length in September was up 3mm from last year. A staple length of greater than 95mm creates challenges for wool processors willing to discount these lots.

A shearer shortage is also compounding delays across heavy wool cutting stock. These delays are only exacerbated by the increase in the national flock.

The Australian Wool Production Forecasting Committee’s September update predicted strong volume growth. The number of sheep shorn is estimated to reach 75 million with wool production set to reach 340 million kg.

This would be longest continuous growth in volumes for the sector since the collapse of the Wool Reserve Price Scheme 30 years ago. The Committee has also forecast average yield and staple strength to increase. These both make Australian wool more competitive.

The Drewry World Container Index – which measures the cost of global shipping – has fallen 61% year-on-year. Easing of shipping costs should provide some relief to wool exporters in Australia. However, they are an indication of a global slowdown in the demand for exported goods.

The World Bank has forecast the Chinese economy to grow by only 2.8% this year. Rising interest rates and the lingering effects of the pandemic will continue to be a challenge for the wool industry.

Sources: Australian Wool Exchange, Australian Wool Testing Authority

Horticulture returns depend on what you grow

For fruit growers, table grape production forecasts have been released by the USDA, and production is expected to increase by 30,000 tonnes to 210,000 tonnes in season 2022-23. This improved production is driven by favourable conditions and greater availability of labour.

Vine plantings are also continuing to mature, further increasing supply estimates. Humid and wet weather impacted the quality of grapes last season which negatively weighed on exports.

As a result, exports are anticipated to rise from 109,000 tonnes in 2021-22 to 130,000 tonnes in 2022-23.

The first trays of this season’s Kensington Pride mangoes have hit store shelves over the last month.

Supply from the Northern Territory will continue to ramp up before peaking towards the end of October. Darwin is forecast to produce 2.6 million trays of mangoes this season compared to 2.4 million in 2021-22.

Katherine mango production is also forecast to increase in 2022-23 to 2.3 million trays, up from 2 million last season.

While labour shortages remain an issue, they aren’t at the same level as the past two seasons.

Meanwhile harvest in the Queensland region of Bowen/Burdekin is set to kick-off by mid-October.

Ongoing rainfall throughout mid-north New South Wales is continuing to impact blueberries. Fungal diseases, driven by persistent rainfall are the primary reason for the reduced output. A third consecutive La Nina is likely to see production impacted through the key summer months.

For vegetable growers, Asparagus production is due to peak during October throughout production regions in Victoria.

Asparagus growers have struggled to absorb the increased production costs seen over the past season. Reduced exports to Japan have also weighed on margins. Strong production driven by favourable conditions and lacklustre export demand are pressuring prices.

September saw the average price drop by $8/kg to $17.50/kg. This downwards trend will continue before prices begin to recover in December as output tapers off.

Lettuce is now coming into key production periods throughout Queensland and Western Australia. An increase in Queensland produce hitting shelves will see prices continue to decline.

This follows the sharp jump in prices seen during June and July when lettuce crops were wiped out by flooding across the Lockyer Vallee in mid-May. Wholesale prices have since dropped from $6.91/kg to just $1.24/kg in September.

For Nut growers the pollination of this year’s almond crop is now essentially complete. This is despite challenges sourcing beehives for pollination following the varroa mite outbreak in New South Wales.

The potential in the crop will be better known in November as nuts begin to mature.

Yields are expected to drop by around 10% in 2023. The maturation of younger almond plantations will help to offset this decline in yield.

This is particularly prevalent around the Griffith region, keeping the Australian crop around 135,000 tonnes.

* The tropical fruit index includes bananas, mangoes, papaws, passionfruit and pineapples.

* * The stem vegetable index includes celery and asparagus.

Sources: Ausmarket Consultants, Rural Bank