Strong export demand keeping grain prices at a historically high level will see growers confident in putting in a full cropping program heading into the 2023-24 season

Winter cereal production is forecast to be the second highest on record this season.

Wheat production will surpass 30 million tonnes for the third consecutive year, for an unprecedented run. While the current estimate of 36 million tonnes is 6% below last year’s record crop, it remains 43% above longer-term averages.

All states are set to produce above average yields. However, crop quality has been impacted by flooding and disease due to record growing season rainfall across east coast growing regions.

In Western Australia the large crop and lower applications of nitrogen due to high prices has led to a lower protein wheat crop which is weighted towards a high proportion of Australian Standard White (ASW) wheat.

The quality profile of the 2022-23 harvest will see a mix of low protein wheat, along with significant supplies of feed quality wheat. The trend in reduced barley area continued this season with planted area down 1% on last year.

As a result, barley production is estimated at 12.8 million tonnes, an 8% decrease on last year.

The United States Department of Agriculture (USDA) reports global wheat production is projected to reach a record 782.7 million tonnes in 2022-23. Global consumption continues to outpace production and is forecast to reach 791 million tonnes.

This has seen annual global ending stocks decline by 3% to 268 million tonnes. This fall in ending stocks is seen across most major exporting nations, including the United States (-15%), European Union (-29%) and Argentina (-31%), which is leading to elevated grain prices.

Where demand expected

Domestic demand for feed grains is projected to strengthen in the first six months of 2023 with cattle production forecast to continue rising.

The feedlot industry continues to demonstrate strong performance with numbers on feed consistently coming in at more than one million head.

Major feedlots are expected to continue utilising wheat as their main feed grain. As a result, domestic consumption of wheat for feed is forecast to increase five per cent from the previous year.

Demand for Australian wheat, especially high protein milling wheat is anticipated to remain strong with total wheat exports of 26 million tonnes forecast for the 2022-23 marketing year.

The ongoing uncertainty surrounding grain exports from the Black Sea combined with the increasing risk involved in exporting from the region will see Australian wheat exports to the Middle East and Africa remain strong.

The drought impacted Argentinian wheat crop has tightened the global production picture further with export estimates for the 2022-23 season now as low as seven million tonnes.

Argentina, the world’s seventh largest wheat exporter, is a direct competitor with Australian exports into the Asian market. This reduced export outlook will see more export demand shift towards Australian wheat.

Barley exports are forecast to fall 7% to around 7.5 million tonnes in 2022-23.

Australia’s recent diversification for malt barley exports into Mexico, Ecuador, and Peru are expected to fall with some export demand reverting to Canada.

Barley production estimates for Canada are up 43.5% from last season’s drought affected crop. This sees their barley exports forecast at three million tonnes versus last year’s two million tonnes.

Early export demand from the Middle East is being seen for Australian feed barley which will continue to support Australian barley exports through the 2022-23 marketing year.

Price to be paid

The delayed harvest and continued uncertainty surrounding the quality of this year’s wheat crop has created some pent-up demand with growers reluctant to sell.

Local Australian Prime Wheat (APW) prices have risen around 20% in the past six weeks to now be trading at parity with international futures prices.

As harvest starts to ramp up, we will see wheat come under selling pressure.

With a near record crop and significant carryover from last season, local prices will fall back below global levels during the key harvest period of December to the end of January.

Once through this harvest period, we forecast prices will rise as Northern Hemisphere supplies dissipate.

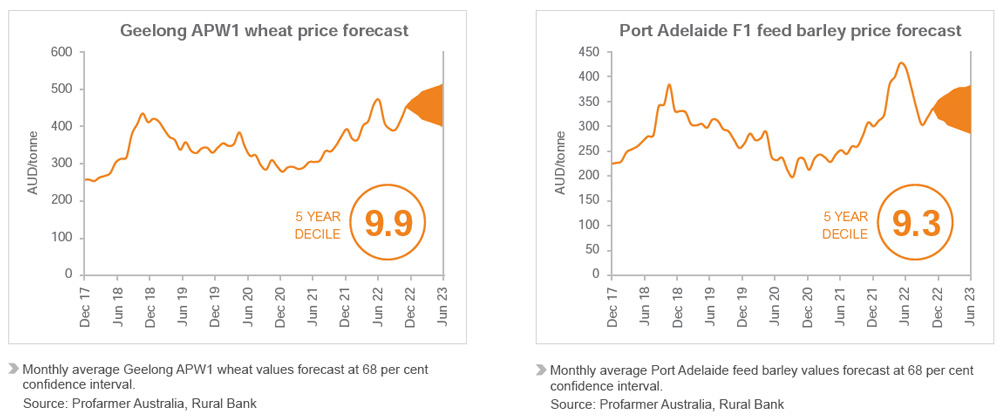

APW wheat prices currently remain elevated at near record decile 9.8 levels. Although this is likely to ease with prices forecast to average $400 per tonne for the first half of 2023.

The unknowns surrounding Black Sea grain supplies will continue to have a big bearing on wheat prices, with any negative or positive news causing large price swings.

Barley prices have gained support from recent moves in wheat and are now back above decile 8 levels. Prices are also finding support from tightening global coarse grain balance sheets.

On the domestic front, barley will likely face growing competition from another season of above average feed wheat production, though will remain viable and competitive into the feed export markets of Asia and the Middle East with global feed grain prices continuing to rise.

This will see barley continue to trade above median prices into 2023 and stay within decile 8 to decile 9 values. In dollar terms this equates to a range of $300-350 per tonne.

Oilseeds in favour

Favourable seeding conditions and high prices saw growers increase area planted to canola by 11% this season.

In Western Australia, the area planted to canola surpassed that of barley for the first time.

Australian canola production estimates of seven million tonnes falls short of last year’s record crop by 2% following crop losses to flooding in Victoria and New South Wales.

The USDA is forecasting global canola production to increase by 15% on last year, largely driven by Canada returning to average production after last year’s drought affected crop.

This rebound in production will see global ending stocks increase 64% to 7.2 million tonnes as supply outstrips demand.

This season is likely to see Australian export market share to India, Asia and Middle East decline as they return to Canadian supply.

Offsetting this is strong export demand from traditional European Union biofuel customers. Demand from Europe could be further enhanced with proposed changes to biofuel mandates in the European Union next year.

Global oilseed production is looking positive for 2022-23 with output forecast to rise 7% to 645 million tonnes. For the most part this rise is driven by an increase in soybean production, but canola has also contributed.

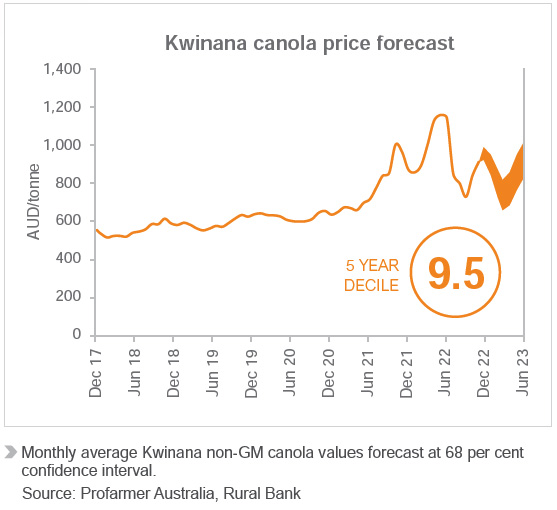

Australian canola prices are not expected to reach the records they saw in 2021-22 due to rising global oilseed supply and easing trade disruptions.

However stable demand from the European Union will put a floor in prices. These supply and demand factors will see Australian canola trade at $680-$810 per tonne during the first half of 2023.

Pulses in firing line

Production of pulses is forecast to decrease 2% down to 2.5 million tonnes this season.

Year-on-year decreases to lentils (-12%), chickpeas (-29%), lupins (-33%), field peas (-9%) and faba beans (-15%) are the result of a combination of decreased planted area, lost crops to flooding, combined with decreased yield from waterlogging and disease due to the wet growing season.

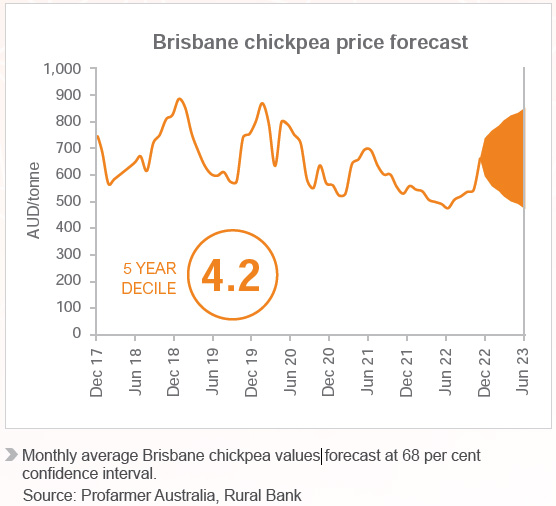

International pulse prices are firming against deepening worries about the yield and quality potential of the Australian crop on account of unusually wet conditions in parts of the country.

Pulse exports for the new season will find some extra support from improving container rates, reliability, and availability. Offsetting these fundamentals for increased pulse prices is an Australian dollar that is expected to appreciate over the next six months.

India is forecast to face tight supplies of domestic kharif (summer) pulses in 2022-23 after summer pulse production came in two million tonnes below government estimates at 8.4 million tonnes.

It is estimated India will import 700-800 thousand tonnes of red and green lentils to make up the shortfall. This will lend support to local lentil prices. However, upside potential will be capped with key competitor Canada having exportable surplus supplies.

Domestic prices for faba beans have firmed in the past month in response to the mixed outlook for the new crop.

Faba bean prices are likely to find continued support from the stock feed industry on concerns of a lack of protein sources as prospects for high protein hay have suffered from flooding with much of the New South Wales and Victorian crop grown on river flats.

Supply for the export market is also starting to look tight. Current export estimates are down 26% on last year to 400,000 tonnes. This should see prices supported in the coming months with a possible 10% upside.