Expected lower milk supply should see high prices sustained in the coming season, but the elevated cost of inputs could keep margins for farmers at the slim end

Australian milk production is forecast to be 6 to 8% below average in the 2022-23 season.

The dairy industry continues to contend with elevated input costs and difficulty accessing labour, while high beef prices continue to encourage destocking of dairy in favour of beef cattle.

A marginal decline in production was already expected before the impacts of flooding interrupted production, transport, and processing activities.

The trend of smaller producers exiting the industry or diversifying farming operations into beef and sheep will persist but is tempered by larger farmers expanding operations or increasing herd sizes.

Cow numbers are expected to fall marginally to around 1.3 million head in 2022-23 but increased yields per cow due to positive seasonal conditions are expected to offset reduced head numbers.

With little indicating significant growth, Australian milk production in 2022-23 is forecast at 8.1 to 8.3 billion litres with further production declines of between 3 to 5% anticipated in the 2023-24 season.

Global milk production is likely to lift slightly in 2022-23 due to improved seasonal conditions in some dairy regions across the EU, New Zealand, and US.

However overall seasonal conditions remain challenging so global production will remain below average and global supply will remain constrained.

Longer term growth will continue to face headwinds in the form of high input costs, farm exits, environmental regulations, and emissions reduction strategies.

Demand is a factor

Domestic demand is expected to remain flat over the first six months of 2023.

Inflationary pressures and increased cost of living are seeing the volume of cheese and higher end processed products like flavoured milks decline.

However, milk is considered a staple item and consumers are choosing cheaper private label products over premium brands rather than reducing overall purchases.

Global demand is expected to weaken slightly in coming months. This is primarily attributed to uncertain demand from China, where increased domestic production has driven an oversupply of whole milk powder while China’s COVID zero policy subdues demand.

A potential squeeze on skim milk powder in 2023 has potential to see some increased demand should EU and US production falter through winter and spring.

Export demand for milk fats is seeing similar consumer dynamics to domestic demand, in that overall demand is expected to remain steady, but will shift to cheaper products like processed cheeses and anhydrous milk fats.

Price race toward record

Farmgate milk prices are currently set at record highs of an estimated $9.30/kg MS with processor prices ranging from $8.85- $10.00/kg MS.

Opening prices in 2023 are forecast to maintain near record levels for the coming season.

Downwards pressure on local prices caused by uncertain and fluctuating global demand and pricing will be offset by ongoing tight global supply, high production costs and the lowest domestic milk pool in over ten years which will see processors competing to secure supply.

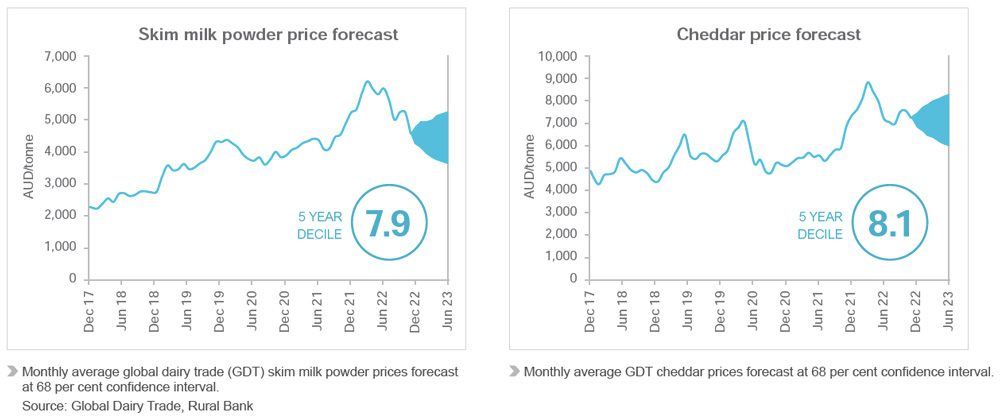

While global prices are anticipated to remain volatile in the face of murky direction from tight supply and uncertain demand, they are likely to be maintained at above average levels.

The trend of milk powder and butter prices easing slightly on softer demand, then gaining value as buyers take advantage of lower prices is expected to continue the trend of volatile but gradually easing global prices.