Good autumn rain in most cropping regions has provided an ideal start for planting this year’s winter crops

Planting of the 2023-24 winter crop is well underway with growers taking advantage of good soil moisture conditions.

Early planted crops have germinated well and are off to a good start. However, growers are watching closely as little rain over the past fortnight is seeing some regions slow down as topsoils dry out.

This will see some planting programs re-evaluated with the possibility of planned canola planting cut back in favour of more cereals.

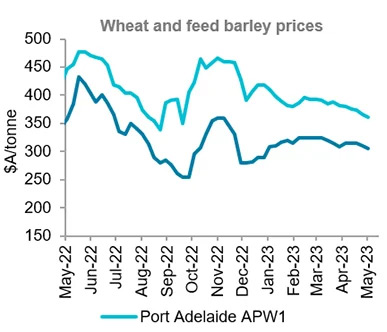

Global wheat markets continued to move lower over the month, dropping US wheat futures by A$34 per tonne, according to a report released by Rural Bank.

Wheat is facing pressure from improved weather conditions in the northern hemisphere. This has led to recent upgrades in the US winter wheat crop ratings.

Other bearish fundamentals for high prices include a forecast 22-year high in the overall Canadian wheat planted area. Two-way market price action remains a strong possibility.

A sudden supply cut from the Black Sea region is one possible catalyst. Production downgrades to the northern hemisphere crop from any adverse weather events is another.

Overall, it looks better for local wheat prices as we didn’t experience the full decline in offshore markets, down by just A$10 to at worst $20 per tonne across port zones over April.

However, trade in our local markets remained quiet as growers focussed on the 2023-24 winter crop planting, and this has limited sell-side pressure.

Local barley markets have remained steady over April. Smaller feedlots are still preferring barley over wheat which is supporting domestic markets.

Export markets have gained some support from the confidence gained by the potential return of exports to China. But there is still much that needs to occur before this becomes a reality.

Canola remains volatile with large price swings over the past month. Any price spikes have been followed by weaker markets which have seen the price for Canola fall by around A$34 per tonne from the previous month.

Export demand for local grain remains strong, with wheat and canola exports at a record pace up to the end of February.

Even with all the confusing rhetoric and feet stomping, China remains Australia’s largest consumer of wheat with a 26% market share of wheat exports. Analysts suggest China is on target to import over seven million tonnes of Australian wheat this season.

Meanwhile, our traditional Asian destinations in Indonesia, Japan, and the Philippines are also strong buyers.