Even faced with outrageous increases in fuel and fertiliser costs growers found it hard to give up their expansion plans and buckled down on a wing and a prayer

The run-up to winter crop plantings for season 2026-27 never looked better with growers coming off the second-best harvest since the record 2022-23 season, with last season producing a meritorious 68.3 million tonnes, albeit from a patchy seasonal run.

With a record Farmgate value of $101.4 billion spilling into farm operations from the 2025-26 season, and with around $54 billion attributed to cropping returns, the 2026-27 season was sitting pretty for growers.

But then the rumbling started, not from dark clouds above but from an unexpected 28 February USA/Israel attack on Iran that killed the country’s leader and with further bombings that followed threw the active shipping lane in the Strait of Hormuz into lock-down.

Growers contemplating how much ground they would plant had plenty to consider, skyrocketing fuel prices and increased fertiliser costs, both rising almost immediately.

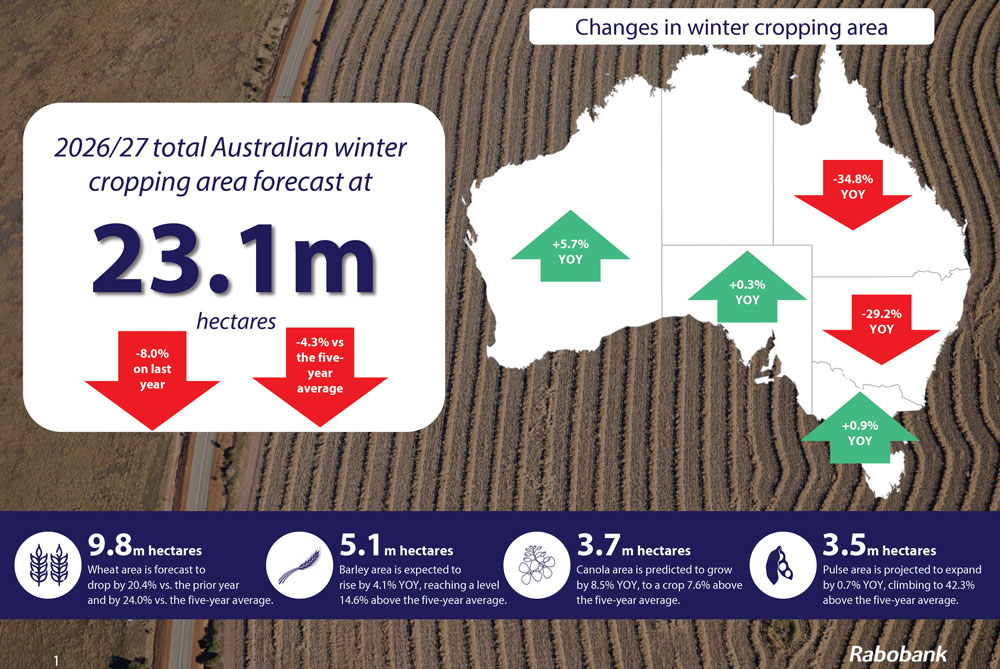

The record 25.1 million hectare planting for season 2025-26 was never going to be achieved and it could have been an almost total disaster, so it comes as somewhat of a surprise that growers buckled down and planted an estimated 23.1 million hectares nationwide for season 2026-27, according to a Rabobank winter crop forecast.

Apart from the significantly higher farm input costs, some growers were also concerned with mixed weather conditions that may affect winter season 2026-27, and not least the likelihood of a severe El Niño event that may reduce rainfall later in the growing season.

To give a recent example of how an El Niño event can restrict a harvest we only need to look at the 2023-24 winter crop when the harvest dropped from 69.2 million tonnes the year before to a devastating 47.5 million tonnes.

Much of the loss in production was felt by marginal cropping areas affected by the dry conditions that spread further south than expected on both the east coast and Western Australia.

Most likely effected in season 2026-27

In its early winter crop forecast, Rabobank, the specialist agribusiness bank estimates winter crop area planting will come in at 23.1 million hectares for the season. That result would represent an 8% reduction on last year and would be 4.3% below the five-year average.

And while most growers would have liked to continue with their crop planting expansion plans, considering everything they needed to consider this season, it was a brave planting.

The decline in cropping area is forecast to affect wheat the most, with nationwide wheat planting estimated to be down by a substantial 20.4% at 9.8 million hectares when compared to last year. A disappointing 24% below the five-year average.

Benefitting from the swing away from wheat was barley, canola and pulse plantings that are forecast to increase on last year’s area, with expectations these crops will offer growers potentially stronger margins than wheat.

Just how the start of the season was perceived varied greatly by growers’ state by state, with Western Australian growers coming off an all-time record harvest last year and full of gusto to plant down a record 9.47 million hectares, up 5.7%.

But in the east, it was a more sombre attitude at play with Queensland growers watching the clouds and obscene input costs to mark down the 2026-27 planting by 34.8% to just 1.06 million hectares.

New South Wales growers took a similar approach to the 2026-27 season with plantings down by 29.2% to just 4.82 million hectares across the state, a big drop on the 6.82 million hectares they put into the ground last year.

While growers in South Australia and Victoria determined to give the season the benefit of doubt to remain relatively stable with planting season from season in South Australia at 3.99 million hectares, up 0.3%. And Victorian growers contributing 3.74 million hectares to the national total, up 0.9%.

Most of this disparity across states can be explained by dry conditions that were experienced early in the season across Queensland and northern New South Wales, while better seasonal starts in Western and South Australia fuelled greater confidence.

Uneven start most noticeable

RaboResearch senior grains and oilseeds analyst Vitor Pistoia digs deeper, “Growers enter the 2026-27 winter cropping season with a more uneven and weather-dependent cropping area than in recent years.

“The season is opening with a clear geographic split across cropping regions. Conditions on the northern east coast, particularly in southern Queensland and northern New South Wales, have been dry through summer and early autumn, leaving limited topsoil moisture and delaying sowing.”

In contrast, Vitor Pistoia explains how Western Australia, South Australia, Victoria and southern New South Wales had entered the season with average to above-average soil moisture, allowing earlier seeding.

This situation included for canola in WA and SA, that was sown as early as late March.

“This marks a reversal from the past two seasons, when eastern regions of Australia held stronger soil moisture at this time and other parts of the country were waiting for the season to break,” Vitor Pistoia explains.

“Recent rainfall that has fallen across some cropping regions in Queensland and New South Wales this month, while beneficial, will not be enough to support a full cropping program, as some regions require up to 100 millimetres of rainfall to replenish soil moisture.”

Looking at the winter cropping season ahead, Vitor Pistoia pondered, there appeared to be a likelihood of “lower growing-season rainfall”, with the high risk of a shift towards El Niño conditions during the winter months and low probability of above-average rainfall across the wheatbelt.

“This means starting-season soil-moisture levels are expected to play a key role in determining yields this season, contributing to greater variability across the cropping belt,” Vitor Pistoia added.

“And with above-average temperatures forecast across many cropping regions for the period, warmer minimums may reduce frost risk, although higher daytime temperatures are likely to increase moisture demand.”

Elevated input costs

Many growers backed off due to elevated farm input costs.

Particularly higher global fertiliser and diesel prices due to the Middle East conflict contributing to increased production costs for growers and influencing cropping decisions.

As a result, higher costs encouraged shifts towards lower-input crops and contributing to a reduction in total cropping area plantings.

While higher input costs are likely to contribute to lower grain production this year, the elevated price of diesel fuel may also reduce the amount of global grain on export markets, Vitor Pistoia expressed, with some regions potentially choosing to supply their local market rather than sending it for export.

“This may potentially slow global grain movements later in the season to ports, providing some underlying support to international grain prices,” Vitor Pistoia concluded.

Crops expected to offer most income

RaboResearch expects grain growers to plant 5.1 million hectares of barleyin season 2026-27, up 4.1% on last year and 14.6% above the five-year average.

It is expected barley markets will remain supported by resilient feed demand, both domestically and across key export markets in Asia and the Middle East.

While global barley stocks remain comfortable following strong 2025 production, tightening supply prospects and steady livestock demand are expected to provide a price floor.

The area planted to canola is projected to be up 8.5% on last season to 3.7 million hectares, a result if achieved 7.6% above the five-year average.

RaboResearch adds, the broader oilseed market globally is supported by strong demand linked to biofuel policies and elevated energy prices, which is keeping canolastocks in check.

The expected expansion in canola cropping area in reflected improved relative returns compared with wheat as well as favourable early-season moisture, particularly in Western Australia and South Australia.

While this additional supply may temper local price upside at harvest, canola continues to benefit from rising global energy prices and biofuel mandates.

Growers are forecast to plant approximately 3.5 million hectares of area to pulsesthis season, including chickpeas, lentils, lupins, peas and faba beans. This is up slightly, by 0.7% on last year, and 42.3% above the five-year average.

RaboResearch indicates India remained the key swing factor in global pulse markets, with expectations of higher Indian import duties, that had been priced into markets in late 2025, yet to materialise.

Global pulse area was likely to expand this season, although at a slower pace than last year.

A developing El Niño raises the likelihood of lower yields both on the east coast, but also in South Asia. As a result, expect prices to remain range-bound, as renewed demand faces headwinds from weaker currencies in key importing countries and higher freight costs, reducing importers’ purchasing power.

For wheat, the RaboResearch report indicated new pricing dynamics were emerging as production is about to drop both domestically and globally.

The global wheat market is shifting from a well-supplied 2025 to a more constrained balance in 2026, driven by higher input costs, weaker profitability and emerging weather risks.

Production and export outlook

In terms of production from the 2026-27 winter cropping season, RaboResearch’s current base case forecast is for approximately 21.3 million tonnes of wheat to be heading for the bins at harvest.

If achieved, this result would be down 41% on the 35.8 million tonnes of wheat produced from the 2025-26 winter crop.

For barley, the current projection is for a harvest of 14.1 million tonnes, and if achieved would be 15% down on last year’s 16.7 million tonnes, despite the increased area planted.

This outlook is due to expected lower yields as a result of dry conditions over NSW and Queensland, lower nitrogen applications rates and the El Niño outlook.

Canola production is projected to reach 6.4 million tonnes, down by 13% on last season’s 7.4 million tonnes, but still in line with the five-year average.

Despite a larger area planted to canola this year, the lower production outlook is driven by the increased likelihood of dry weather conditions over the pod filling period due to the prospects of an El Niño event.

The report indicated exports for the 2025/26 season to date are broadly on track to avoid a significant carryover of grain and oilseeds stocks building up for the season ahead.

For the first six months of the 2025-26 season, October to March, wheat shipments had reached 12.6 million tonnes, in line with the pace to meet the full-year export program.

Barley exports had been strong at 6.4 million tonnes, largely driven by demand from China. In contrast, canola exports for the period were approximately 0.3 million tonnes under recent years’ average, reflecting a recovery in European stocks and weaker import demand.

Looking ahead, alongside policy developments, rising fuel costs are likely to become an increasingly important driver in the global trade outlook, the report concluded.